Commercial Term Index – 2025.

With Savills forecasting the Commercial Term investment market to reach approximately £55bn in 2026, and a refinance market of a similar size, we decided it was an opportune time to dive into the numbers, analyse the deals that we and some of our broker partners saw in 2025, and highlight some of the recent trends and opportunities that may lie ahead.

Thanks to Aria Finance, B2B Finance, Clever Lending, Synergy Commercial Finance and Watts Commercial Finance for their support collating the data set of almost 2400 commercial term cases.

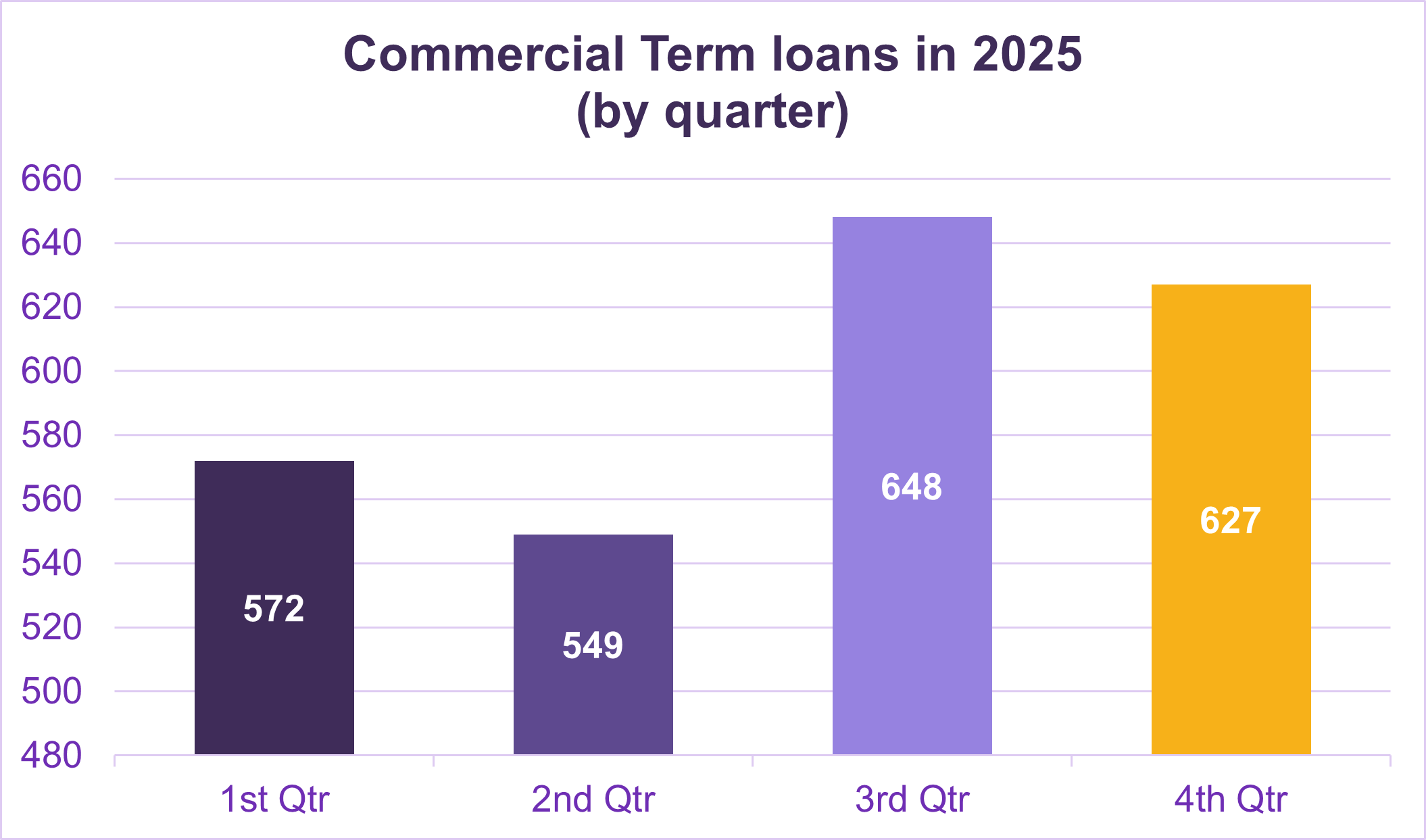

Commercial Term loans in 2025 by quarter

After a sluggish first half of 2025, momentum steadily built back up with more Commercial Term deals completed as confidence slowly returned.

The Autumn Budget looked like it had the potential to derail that momentum, but a more positive than expected statement helped to support a strong end to 2025.

| Quarter | No. of Commercial Term cases | % of Commercial Term lending |

|---|---|---|

| Q1 - 2025 | 572 | 23% |

| Q2 - 2025 | 549 | 21% |

| Q3 - 2025 | 648 | 29% |

| Q4 - 2025 | 627 | 27% |

Based on 2396 qualifying Commercial Term cases completed in 2025 by Together, Aria Finance, B2B Finance, Clever Lending, Synergy Commercial Finance and Watts Commercial Finance.

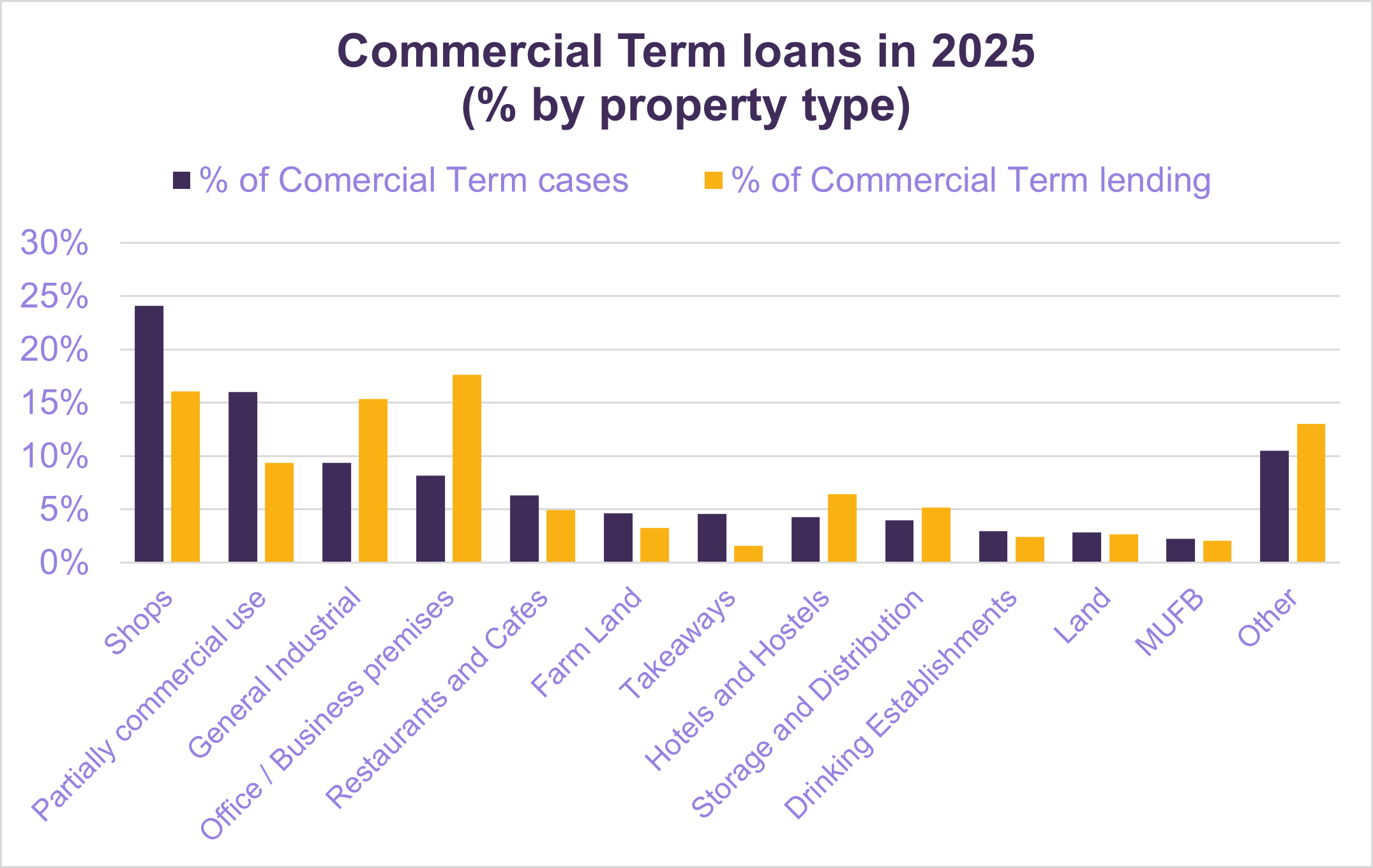

Commercial Term loans in 2025 by property type

Based on data from Together’s Commercial Term deals throughout 2025, it’s clear that shops and semi-commercial properties remain specialisms with consistent demand, representing ~40% of the market quarter on quarter.

The hospitality sectors and low occupancy office properties also show an appetite, indicating that many investors are keen to capitalise on potentially below market value assets.

Cost challenges facing the retail and food sectors may have also impacted the rise in restaurant and café asset classes throughout the year as some business operators closed.

| Property Type | % of Commercial Term cases | % of Commercial Term lending |

|---|---|---|

| Shops | 24% | 16% |

| Partially commercial use | 16% | 9% |

| General Industrial | 9% | 15% |

| Office / Business premises | 8% | 18% |

| Restaurants and Cafes | 6% | 5% |

| Farm Land | 5% | 3% |

| Takeaways | 5% | 2% |

| Hotels and Hostels | 4% | 6% |

| Storage and Distribution | 4% | 5% |

| Drinking Establishments | 3% | 2% |

| Land | 3% | 3% |

| MUFB | 2% | 2% |

| Other | 11% | 13% |

Based on 1598 qualifying Commercial Term cases completed in 2025 by Together (where asset type and lending amount was visible).

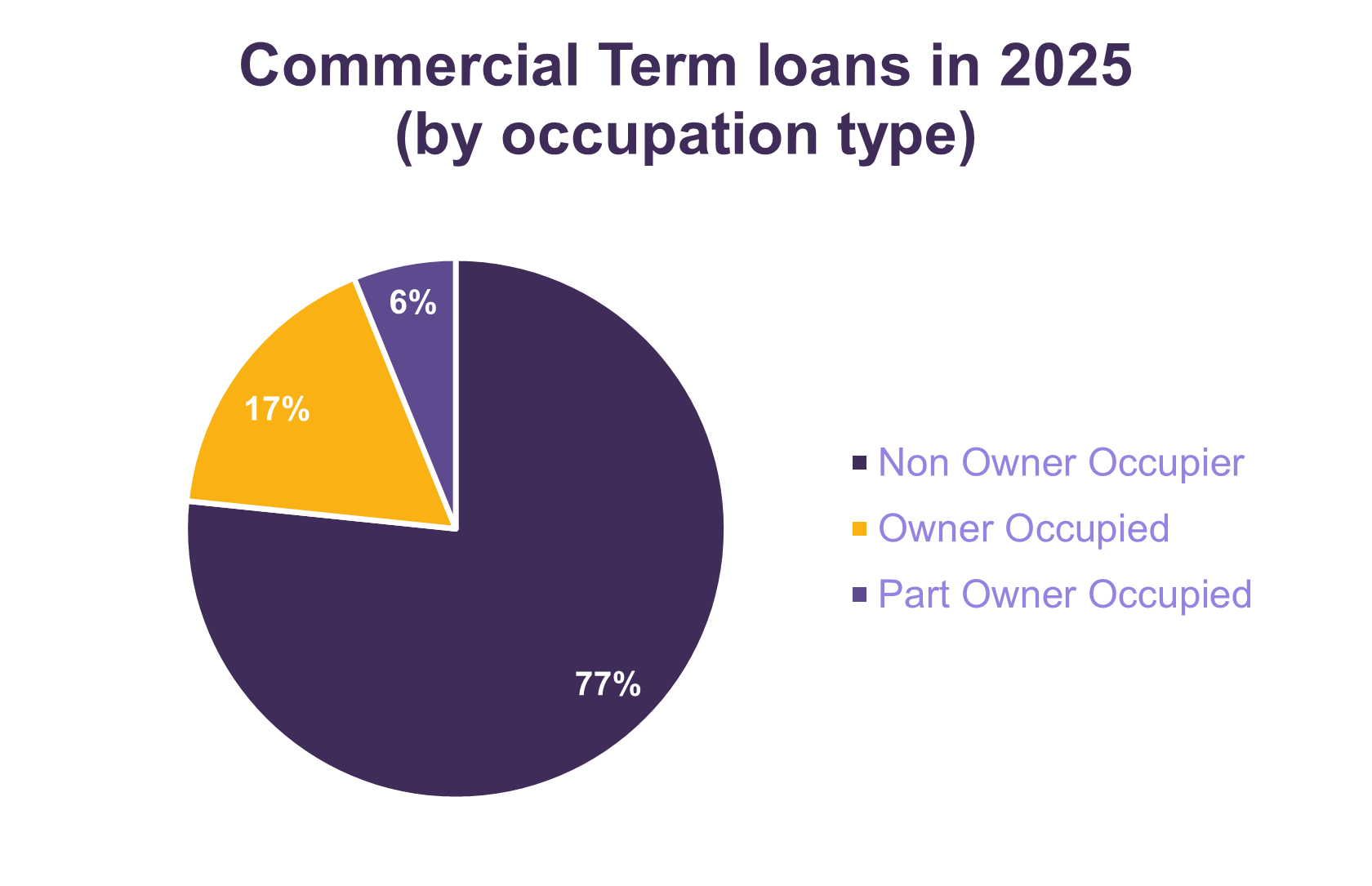

Commercial Term loans in 2025 by occupier status

Our data also shows that a majority of clients (77%) using a commercial term in 2025 were non-owner occupiers, indicating that investor demand in commercial properties remains high. Many Buy to Let residential investors have pivoted to commercial property, attracted by good yields, undervalued assets, and of course, a less punitive Stamp Duty Land Tax cost.

However, the year ended with rise in business owners looking to acquire premises to operate from, suggesting an improving sentiment looking ahead to 2026. This may partly be fuelled by some landlords reviewing their portfolios and disposing of non-performing assets and offering the purchase opportunity to existing tenants.

| Status | % |

|---|---|

| Non Owner Occupier | 77% |

| Owner Occupied | 17% |

| Part Owner Occupied | 6% |

Based on 1875 qualifying Commercial Term cases completed in 2025 by Together, Aria Finance, B2B Finance, Clever Lending, Synergy Commercial Finance and Watts Commercial Finance (where occupier status was visible).

Loan size activity

Whilst the specialist space is equally at home providing hundreds of loans between £1m and £20m, what is clear is that the SME community is heavily reliant on specialist lenders in the smaller loan space, with 65% of all activity below £250k and over 80% of activity under £500k.

Loan sizes increased through the year as the market benefited from a downward rate environment.

Commercial Term loans in 2025 by region

Regionally, the North West of England leads the way for the number of Commercial Term mortgages we completed in 2025. However, London and the South West continued to dominate on the amount of borrowing, with higher property prices and larger transactions prevalent.

| Region | % of Commercial Term cases | % of Commercial Term lending |

|---|---|---|

| Scotland | 8% | 9% |

| North East | 5% | 3% |

| Yorkshire and Humber | 12% | 14% |

| North West | 18% | 16% |

| Wales | 6% | 4% |

| West Midlands | 11% | 9% |

| East Midlands | 5% | 4% |

| East Anglia | 6% | 5% |

| South West | 6% | 5% |

| London | 6% | 15% |

| South East | 15% | 16% |

Based on 1890 qualifying Commercial Term cases completed in 2025 by Together, by Together, Aria Finance, B2B Finance, Clever Lending, Synergy Commercial Finance and Watts Commercial Finance (where location status was visible).

General commentary

Savills reported that a strong Q4 helped deliver a total UK investment market of around £54bn in 2025. Applying a 60% LTV filter to those investment volumes gives a more realistic view of the debt that might be available in the market.

Overseas investors continue to dominate the larger transaction space, accounting for up to 60% of activity and typically big ticket deals. When they need funding, it is usually provided by a mix of private credit and senior lenders. On the refinance side, most of the activity sits in large loans, where many high street banks and ambitious challengers have leaned towards a “pretend and extend” approach.

Despite these shifts at the top end, overall transaction levels in 2025 were broadly flat. This suggests that activity in the specialist market, including kerbside and smaller commercial assets, has remained resilient.

Industry sentiment

Early 2026 started off positively throughout the specialist lending market, with expectations of a downward rate trajectory giving brokers, lenders and investors cause for optimism.

However, the turbulence caused by the war in the Middle East and rising oil prices will only add to inflationary pressures dampening sentiment and delaying some activity. The Bank of England’s base rate decision in March, holding at 3.75%, looks to be cautious but pragmatic, but rising swap rates are causing lenders across the market to reevaluate their pricing.

A weakening of activity seems likely over the next few month as debt costs rise although it may lead to an increase in forced sales and Below Market Value opportunities. The more cautious high street banks and other senior lenders may reign back appetite to see how the conflict plays out, providing opportunity for the specialist market.

Regardless, there’s still opportunities in the market for investors as capital values continue to recover and other investors refresh their portfolios, selling assets that no longer fit their business plans.

Additionally, assets such as Purpose Built Student Accommodation, prime office space and Industrial and warehousing sectors continue to grow due to demand and scarcity.

If you have a commercial term case that you’d like to discuss with us, please get in touch with our expert team.

Get in touchSimilar Articles

-

£13 million commercial loan helps Turkish wholesaler chain refinance and reinvest

2 minBusinessIntermediariesMortgage -

Derelict to Destination: Commercial bridging loan supports Preston hotel regeneration

3 minBusinessIntermediariesBridging Loan -

£7.9m commercial term loan secures time-sensitive deal for a Scottish office block

2 minBusinessIntermediariesSecure Loan

Any property, including your home, may be repossessed if you do not keep up repayments on your mortgage.

All lending decisions are based on lending criteria and, where applicable, subject to credit check and an assessment of individual circumstances.

All mortgages are subject to our terms and conditions.

Loans offered by Together Commercial Finance Limited are not regulated by the Financial Conduct Authority.

Articles on our website are designed to be useful for our customers, and potential customers. A variety of different topics are covered, touching on legal, taxation, financial, and practical issues. However, we offer no warranty or assurance that the content is accurate in all respects, and you should not therefore act in reliance on any of the information presented here. We would always recommend that you consult with qualified professionals with specific knowledge of your circumstances before proceeding (for example: a solicitor, surveyor or accountant, as the case may be).